Introduction

If you’ve recently opened your renewal notice and asked why is my car insurance going up, you’re not alone — millions of drivers across the U.S. are seeing the same thing in 2026.

The Big Picture: Is Car Insurance Going Up in 2026?

Yes — car insurance is going up in 2026 for most Americans. According to the U.S. Bureau of Labor Statistics, auto insurance costs rose over 20% in recent years, and 2026 continues that trend. Insurers are adjusting to a new economic reality driven by inflation, climate events, and technology costs.

The average annual premium in the U.S. now exceeds $2,100, up from around $1,600 just three years ago.

| Year | Average Annual Premium | YoY Change |

|---|---|---|

| 2022 | $1,630 | +4% |

| 2023 | $1,900 | +16.6% |

| 2024 | $2,050 | +7.9% |

| 2025 | $2,100 | +2.4% |

| 2026 (est.) | $2,200+ | +4–6% |

Source: Insurance Information Institute estimates

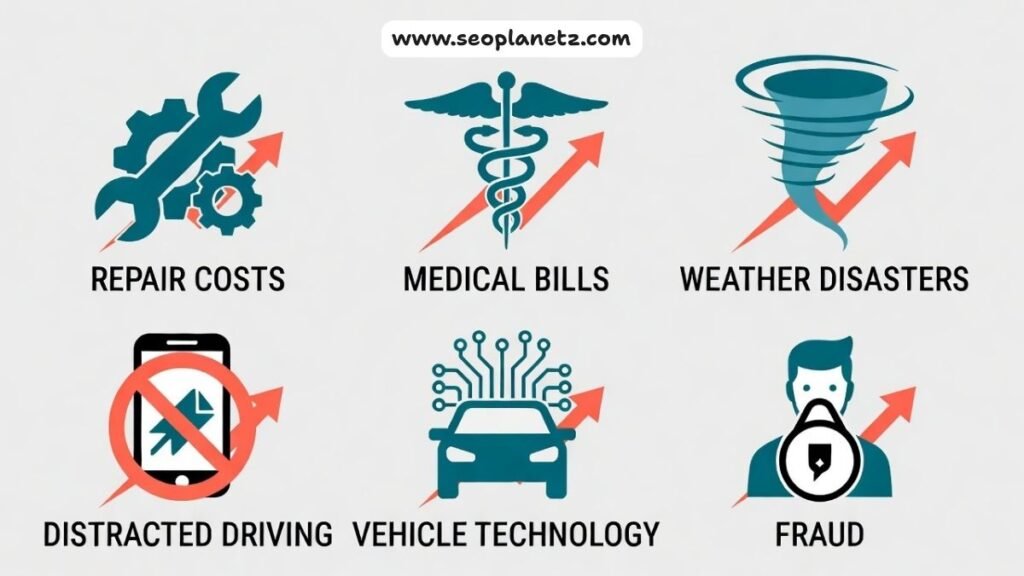

Top Reasons Why Your Car Insurance Keeps Going Up

1. Inflation Is Hitting Repair Costs Hard

Car parts, labor, and replacement vehicles all cost more. A fender bender that cost $1,200 to fix in 2019 now costs $2,400+. Insurers pay those bills — and pass the cost to you.

The National Highway Traffic Safety Administration (NHTSA) reports that modern vehicles with ADAS (advanced driver assistance systems) cost significantly more to repair than older models.

Also Read: Alternator Failure Reasons and Solutions in 2026

2. More Expensive Vehicles on the Road

Electric vehicles and tech-loaded cars have sensors, cameras, and specialized parts everywhere. Even minor accidents trigger expensive repairs. This raises claims costs industry-wide — even for drivers of older vehicles.

3. Medical Cost Inflation

Liability claims involve medical expenses. As healthcare costs rise, so does the bodily injury payout on every claim. The Centers for Medicare & Medicaid Services estimates healthcare spending grows 5–7% annually.

Why Does My Car Insurance Keep Going Up With No Accidents?

This is the most common complaint — and it’s completely valid. Your driving record isn’t the only factor insurers consider. Here’s why your rate rises even with a clean record:

- Your ZIP code changed risk profile — rising crime or accidents in your area affect everyone

- Statewide rate filings — insurers file blanket increases approved by state regulators

- Your vehicle aged into a higher-risk bracket

- Credit score fluctuations (in states where allowed)

- Uninsured motorists increased in your region

According to the Insurance Information Institute, roughly 1 in 7 drivers is uninsured. When they cause accidents, insured drivers’ rates absorb the cost.

Also Read: Car Battery Draining Fast Reasons and Solutions in 2026

Why Did My Insurance Go Up for No Reason? (Hidden Triggers)

Sometimes the reason feels invisible. These are the silent rate triggers most people miss:

| Hidden Trigger | Impact on Premium | How to Check |

|---|---|---|

| Credit score drop | +10–25% | Request CLUE report |

| New household driver added | +15–40% | Review policy declarations |

| Lapse in coverage (even 1 day) | +10–20% | Check renewal dates |

| ZIP code reclassification | +5–15% | Ask insurer directly |

| Vehicle safety rating change | +3–10% | NHTSA vehicle ratings |

| Increased local claim frequency | +5–20% | State insurance dept. data |

Why Is My Car Insurance Going Up in California?

California drivers face a unique crisis. Why is my car insurance going up in California so dramatically? Several state-specific factors are at play:

Wildfire Risk — Insurers are repricing risk statewide after massive wildfire losses. Even auto policies are affected as total-loss claims spiked.

Proposition 103 Delays — California requires regulatory approval for rate increases, which created a backlog. Now that approvals are clearing, insurers are implementing years of pent-up increases at once.

Major insurer exits — When large carriers leave a market, remaining insurers face less competition and more concentrated risk.

The California Department of Insurance provides a rate comparison tool for residents shopping for better deals.

Why Does My Car Insurance Keep Going Up Every 6 Months?

Most policies renew every 6 months — and each renewal is a fresh pricing opportunity for insurers. Here’s the renewal cycle reality:

Every 6 months, insurers re-run your profile against:

- Updated credit data

- New regional claims statistics

- Current repair cost indexes

- Your updated driving record

- Industry-wide loss ratios

Even a 3% increase every 6 months compounds to 6%+ annually — which adds up fast over several years.

Also Read: 2026 Chevy Silverado Specs & Prices

Why Does My Car Insurance Keep Going Up Every Month?

If your bill changes monthly, you’re likely on a monthly payment plan. Insurers often add installment fees. Alternatively, a mid-term endorsement change triggered a recalculation. Always check your declarations page for itemized charges.

The Distracted Driving Effect

Accident rates are climbing despite better vehicle safety tech. Distracted driving — primarily smartphone use — caused over 3,500 deaths in 2022 according to NHTSA data. More accidents mean more claims. More claims mean higher premiums for everyone.

Also Read: How to Jump a Car Safely and Correctly in 2026

How to Stop Your Car Insurance From Going Up

You have more control than you think. Here are proven strategies:

Shop Around Aggressively Get car insurance quotes from at least 3–5 insurers every renewal. Loyalty rarely pays. Sites like the National Association of Insurance Commissioners (NAIC) can help you find licensed insurers in your state.

Increase Your Deductible Raising your deductible from $500 to $1,000 can cut your premium by 15–30%. Only do this if you have savings to cover it.

Bundle Policies Combining home and auto insurance with one carrier typically saves 10–25%.

Improve Your Credit Score In most states, a better credit score directly lowers your premium. Pay down balances and avoid new hard inquiries before renewal.

Also Read: Why Is My Car Smoking? 7 Common Causes and How to Fix Them

Take a Defensive Driving Course Many insurers offer discounts of 5–15% for completing an approved course. Check with your state DMV for approved programs.

Drop Unnecessary Coverage on Old Cars If your car is worth under $4,000, comprehensive and collision coverage may cost more than the car’s value.

Key Takeaways

- Why is my car insurance going up comes down to inflation, more expensive vehicles, rising medical costs, and increased accident frequency

- Even with no accidents, your rate can rise due to ZIP code changes, credit shifts, or statewide filings

- California drivers face compounded increases from wildfire risk and regulatory backlogs

- Every 6-month renewal is a re-pricing event — insurers update all your risk factors

- Shopping around at every renewal is the single most effective way to fight increases

- Bundling, higher deductibles, and credit improvement all reduce premiums

- Cheap car insurance exists — but you have to actively look for it; loyalty discounts rarely offset market increases

Frequently Asked Questions

Q: Why did my car insurance go up if nothing changed?

A: Even without personal changes, insurers apply regional rate adjustments, updated credit data, and industry-wide loss calculations at renewal. Your personal record is just one factor among many.

Q: Why is my car insurance going up every year consistently?

A: Annual increases reflect cumulative inflation in repair costs, medical expenses, and claims frequency. Most U.S. drivers see 4–8% increases per year in the current environment.

Q: Why does my car insurance keep going up every 6 months?

A: Six-month policies renew with fresh pricing. Insurers reassess your full risk profile at each renewal, meaning any change in credit, regional data, or loss ratios can push your rate up.

Also Read: 2024 Ford Bronco Raptor Specs & Prices

Q: Why is car insurance increasing so dramatically in 2026?

A: The 2026 increases are the result of several overlapping factors: post-pandemic parts inflation, EV repair complexity, climate-related losses, and rising medical costs all hitting simultaneously.

Q: How can I avoid insurance increases?

A: Shop multiple carriers every renewal, maintain good credit, bundle policies, raise your deductible, and ask your insurer about every available discount — including telematics/usage-based programs.

Q: Why did my insurance go up with no warning?

A: Insurers are required to send renewal notices, but rate change notifications can be buried in the paperwork. Always read your renewal declarations page and compare it to your previous one line by line.

Q: Why is health insurance going up in 2026 alongside auto insurance?

A: Both are driven by the same root cause — rising healthcare and service costs. Medical inflation affects bodily injury claims in auto policies and directly drives health insurance premiums simultaneously.

Conclusion

Understanding why is my car insurance going up is the first step to doing something about it. In 2026, rising premiums aren’t personal — they’re systemic. Repair costs, medical inflation, distracted driving, and climate events have all combined to push the entire industry upward.

But you’re not powerless. When you know why is my car insurance going up, you can take targeted action: compare car insurance quotes aggressively, adjust your coverage, improve your credit, and ask the right questions at renewal. Small changes can save hundreds of dollars annually.

Don’t accept every increase passively. Review your policy, shop the market, and use every tool available to keep your costs manageable — because why is my car insurance going up has real answers, and those answers point toward real solutions.